This week will continue to be dominated by developments in the Middle East. On Friday, the US and Israel struck Iran’s nuclear and missile facilities, and Iran retaliated across the Persian Gulf, as President Trump pushed for a deadline for Tehran to reopen the Strait of Hormuz or face further attacks on its infrastructure. The increase marked a sharp change in tone from earlier in the week, when financial markets were volatile after Trump’s panic led to threats targeting Iran’s energy facilities.

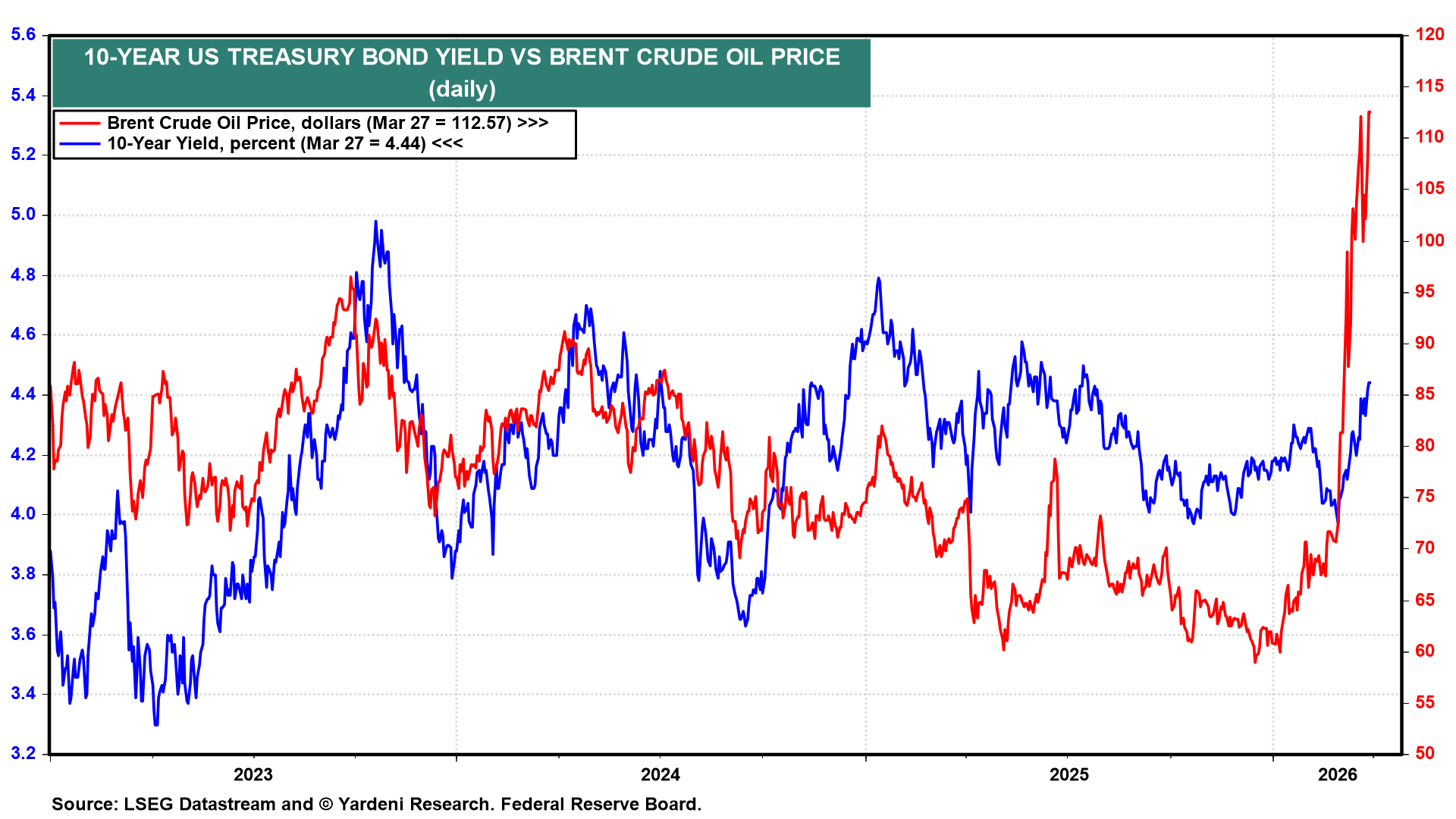

Oil markets have responded accordingly. WTI closed at $99.64 a barrel, up 18.7% from Tuesday’s low of $83.96 and marking its highest weekly close since the conflict began, while Brent ended at $112.57, up 16.6% from its weekly low of $96.52 (chart). The speed and magnitude of the move make it clear how quickly energy markets are reacting to environmental risk, challenging earlier efforts to keep oil and bond markets stable, and heightening the risk of further disruption in the Strait.

Because of that, this week’s scores will have extra importance. A heavy slate of releases, including consumer confidence, PMIs, and the March jobs report, will provide the first meaningful reading on how high energy prices and growing uncertainty are weighing on the real economy. The key question is whether the stability of the US economy can withstand this shock, or whether cracks are beginning to appear in jobs, attitudes and the labor market.

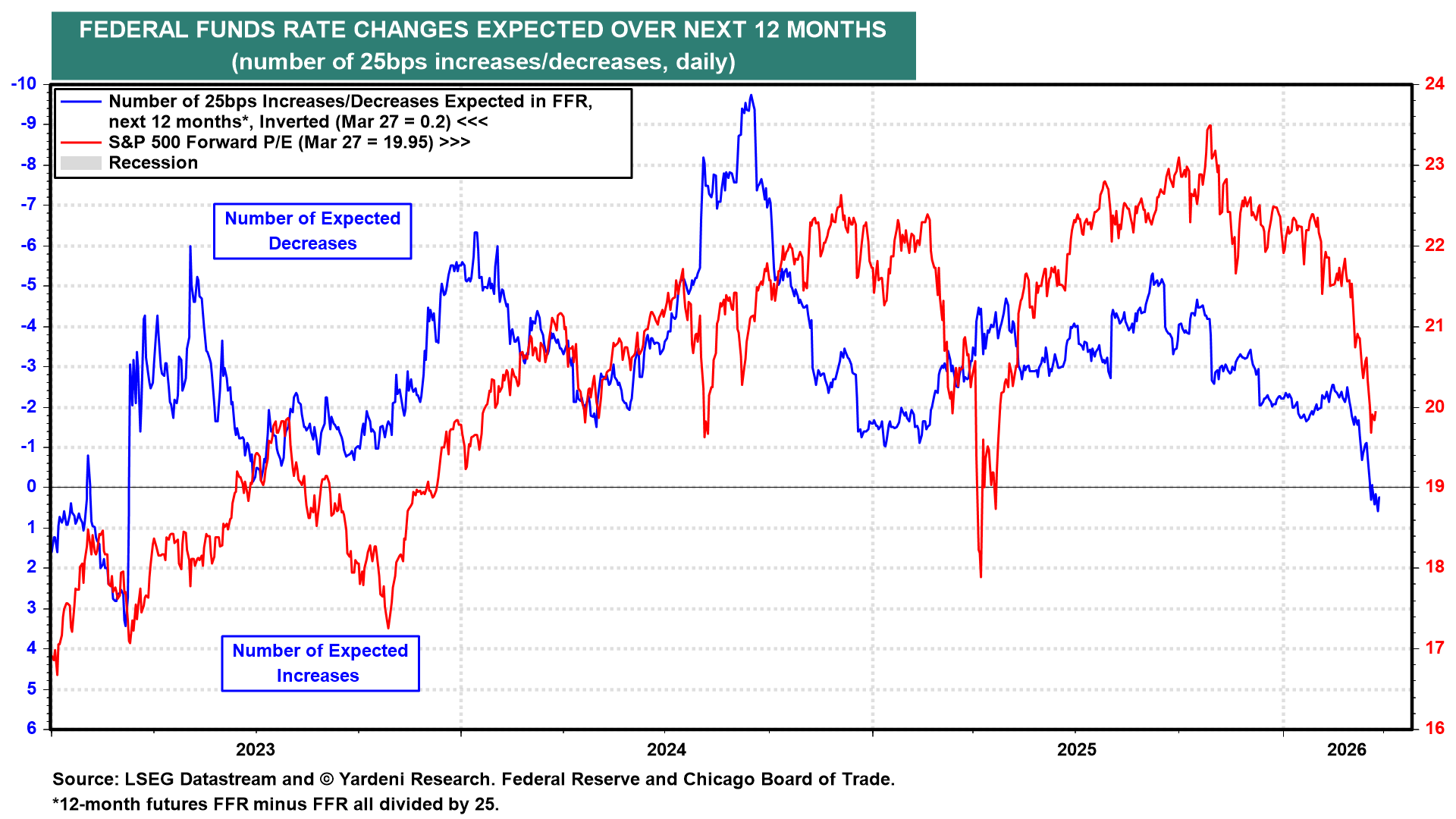

As tensions continue and energy prices rise, rate hikes are being pushed back on the horizon, and there is still a lot of weight on the valuation figures (chart).

Here are key U.S. economic data that will likely shape investors’ thinking on the labor market, the outlook for growth, and the path of fiscal policy this week:

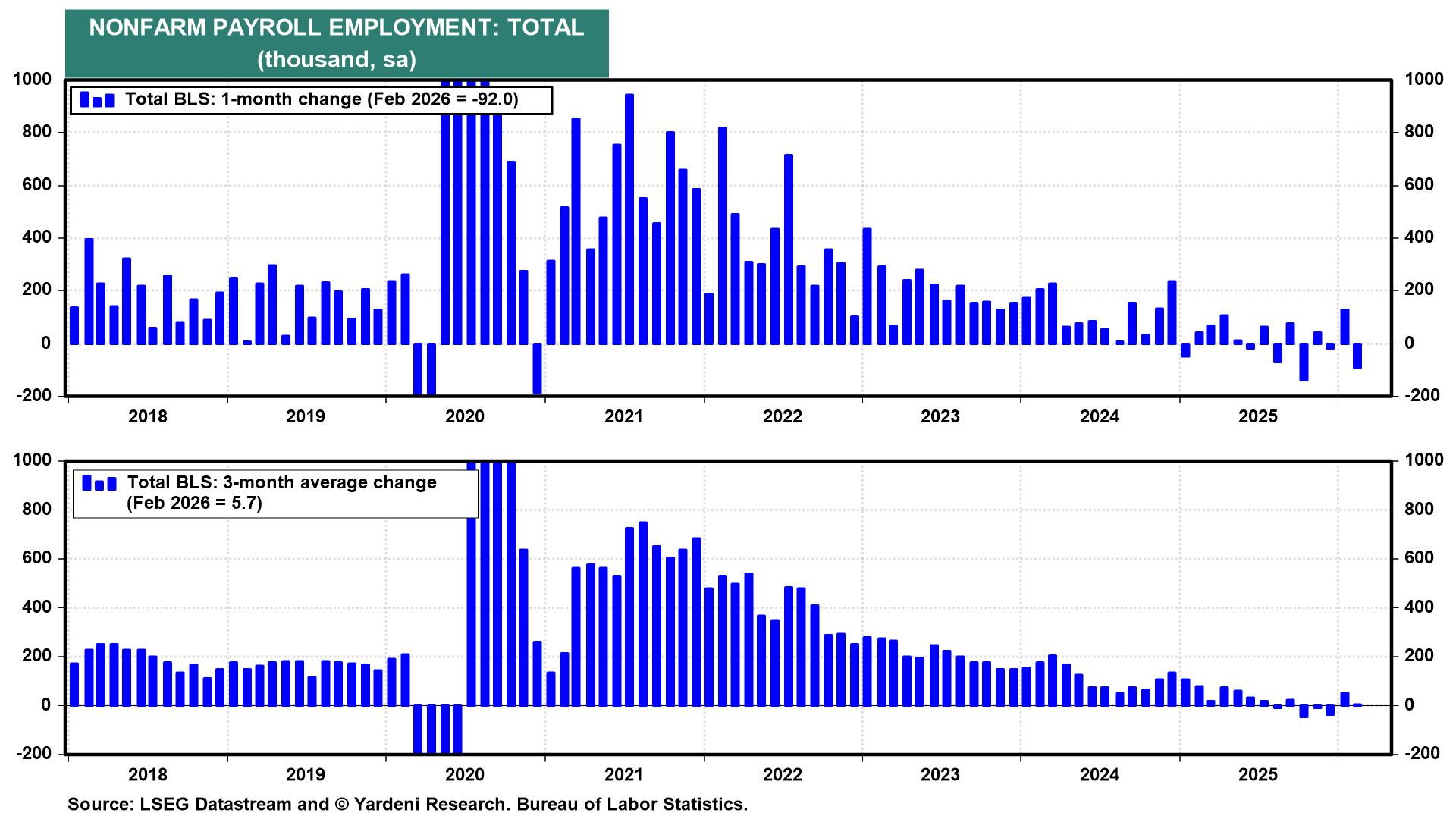

(1) Work. The March (Friday) payrolls report will have added significance after February’s unexpected drop of 92,000 and a rise in the unemployment rate to 4.4%. Bloomberg’s median estimate is for an increase of 60,000, and no forecasters expect job losses, suggesting that the labor market remains strong despite the low levels. We will also receive additional signals from ADP (Wed), Challenger (Thu), and weekly unemployment reports (Thu), which should help clarify whether February’s weakness was a one-off or the start of a larger decline.

Earnings growth has already shown signs of losing momentum, with monthly gains becoming erratic and the three-month average falling (chart).

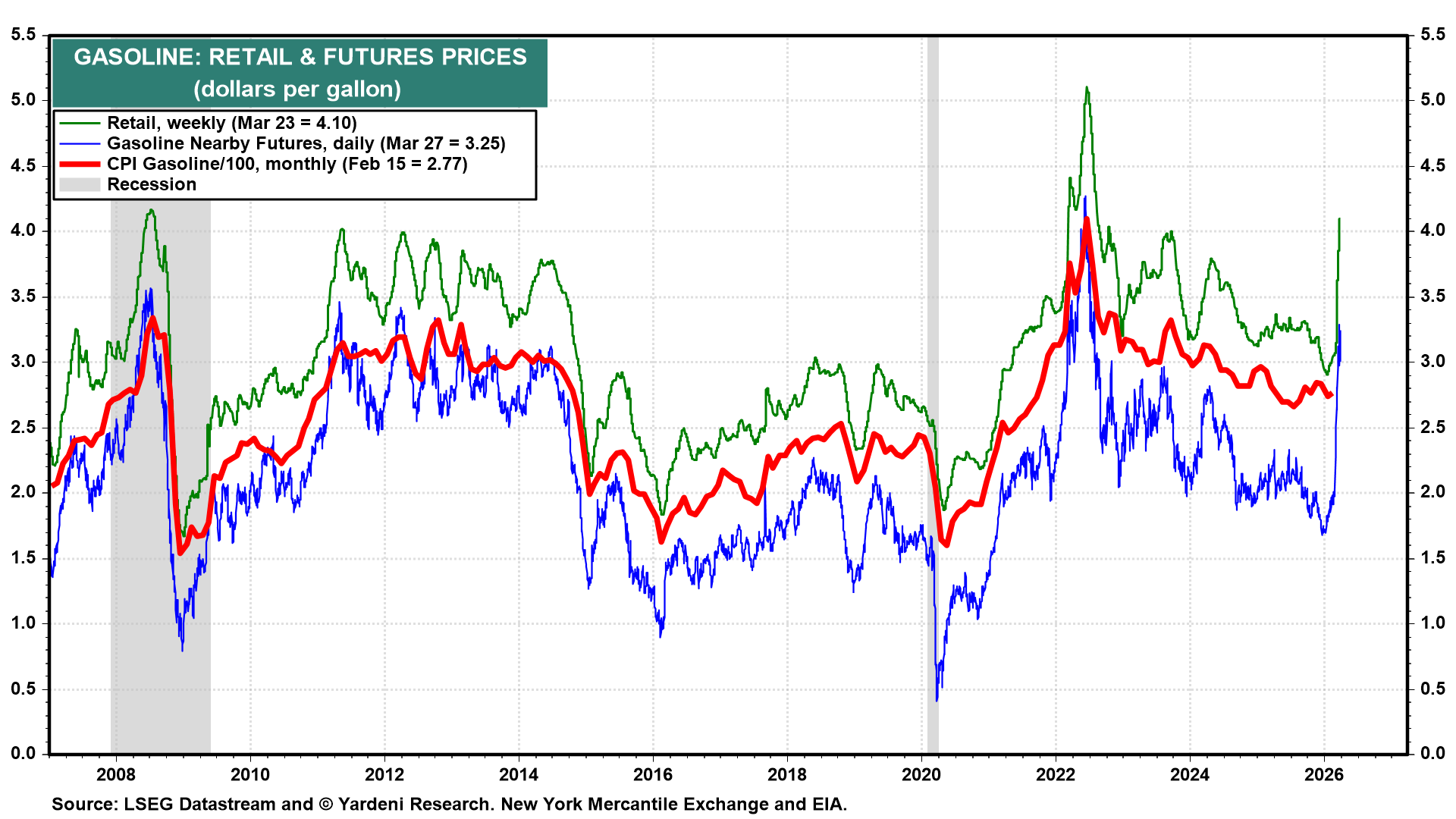

(2) Consumer confidence. Consumer confidence will be closely watched this week as one of the first numbers to gauge how rising electricity prices are affecting households. National gasoline prices rose from $2.98 on February 26 to $4.10 per gallon on March 23, an increase of about 38% that could weigh on consumer sentiment (chart).

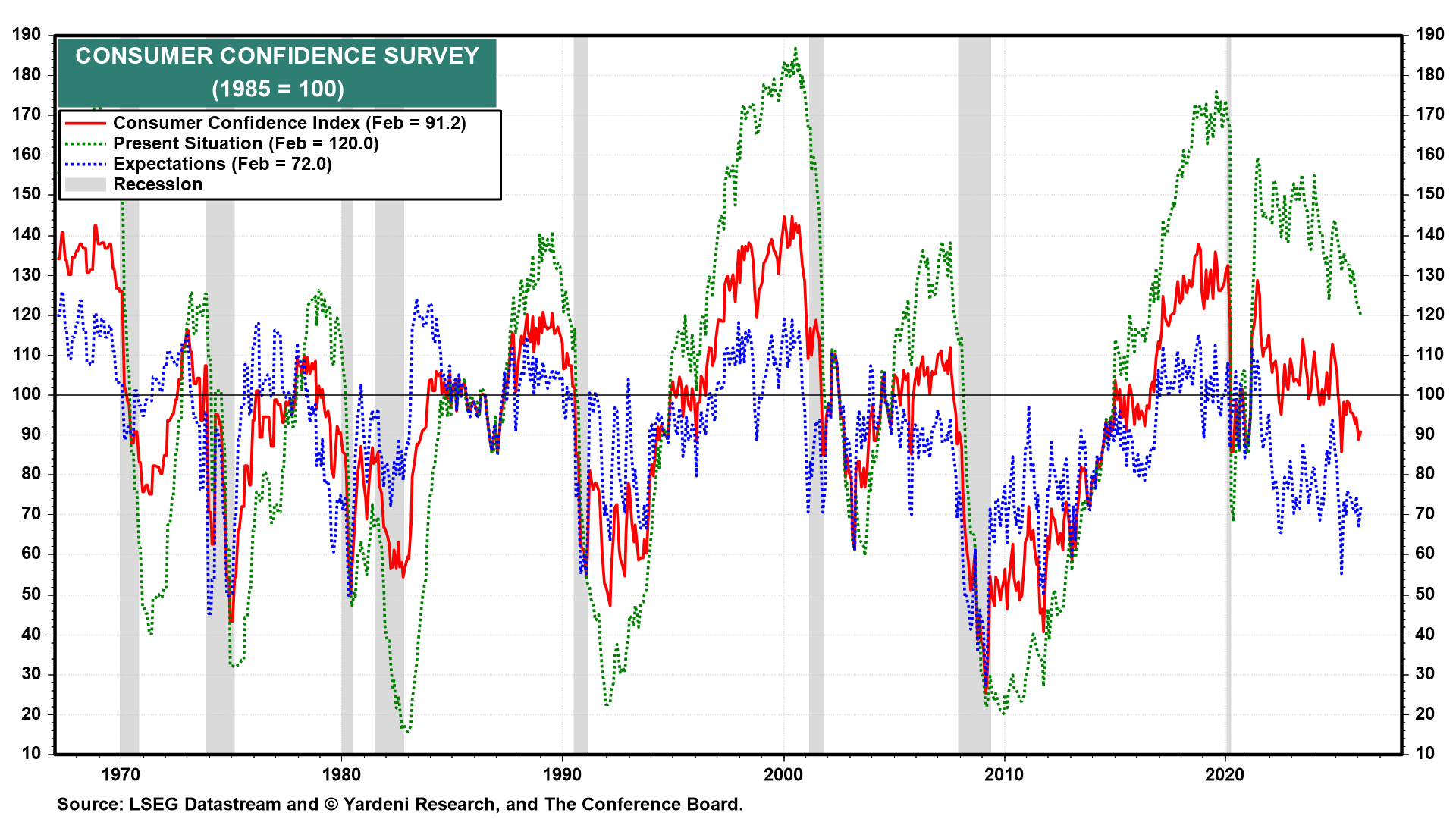

Since July, headline confidence has been falling, and expectations have been significantly reduced (chart). This should continue. We will focus mainly on the outlook due to the possibility that high petrol prices will continue in the coming months.

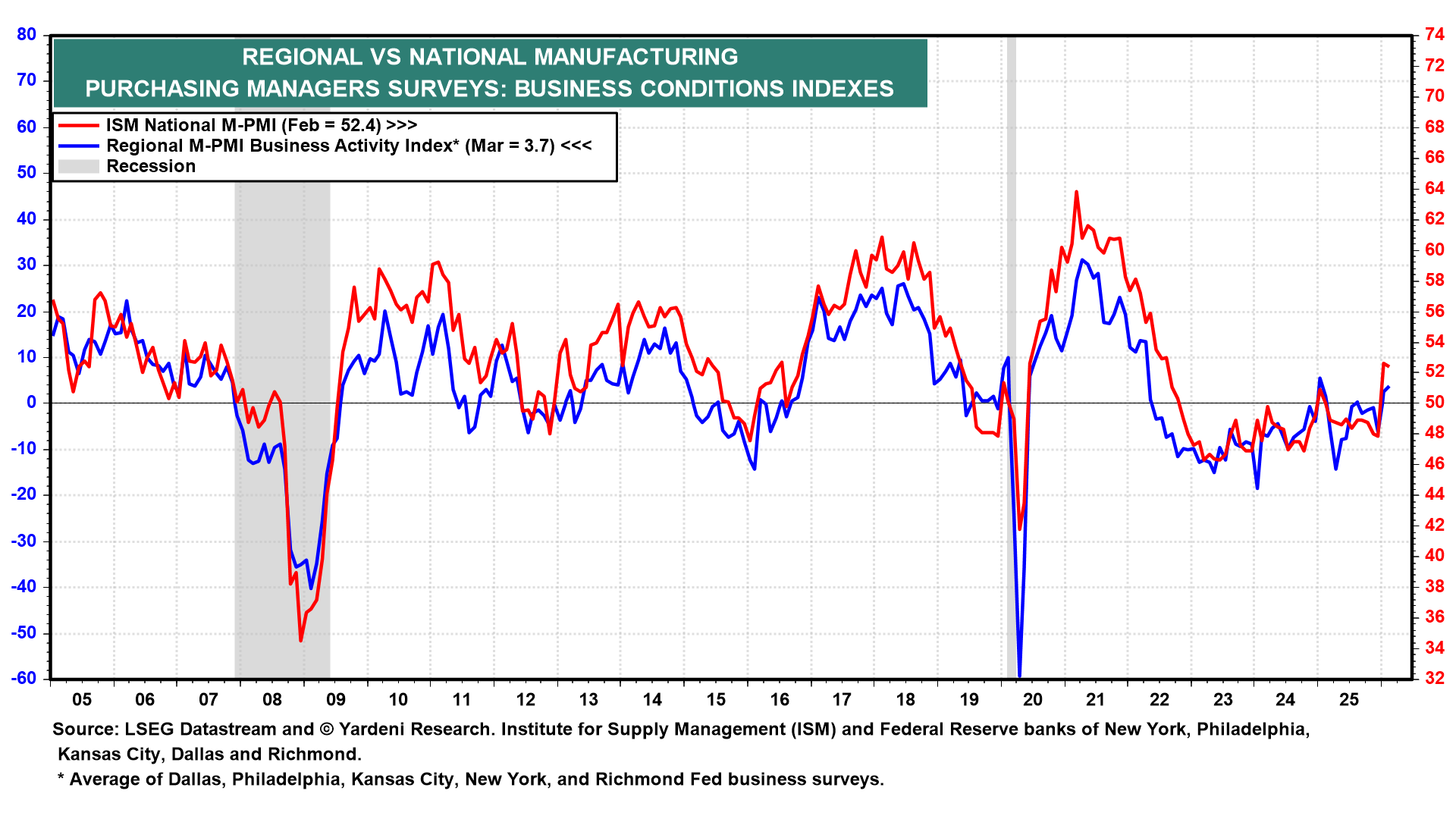

(3) PMIs. Manufacturing data will be in focus this week, with the Chicago PMI, final S&P 500 PMIs, and ISM output due. With uncertainty raised by rising oil prices and the Fed’s policy buying, forward-looking sectors will be important. The regional survey for March remained soft in relation to the expanding ISM, highlighting the difference between the weak regional performance and the national reading (chart). If the ISM begins to converge to a lower number of regions, it may suggest that the development of production is losing momentum after a period of stability.

💡

Have a chat with Ed below! To leave comments or questions, visit the Yardeni QuickTakes website and post them at the end of the QuickTakes article. Contributions of paid members can be presented in our section, “Ed Answers Your Questions”.

#UPCOMING #ECONOMIC #WEEK #March #30April