The impending freeze will highlight the precarious situation of many developing economies that until last month were enjoying rising demand for their debt, rising tariffs and other political turmoil.

Register Here.

The one exception this month has been a rally in oil-producing Angola, fueled by a greenback spike.

“All financing discussions are ongoing but with a cautious wait-and-see approach,” Victor Mourad, Citi’s co-head of CEEMEA debt financing, told Reuters.

“There is access for suppliers, especially large suppliers if needed, but that access comes at a high price,” he said.

TOWARDS THE DAYS

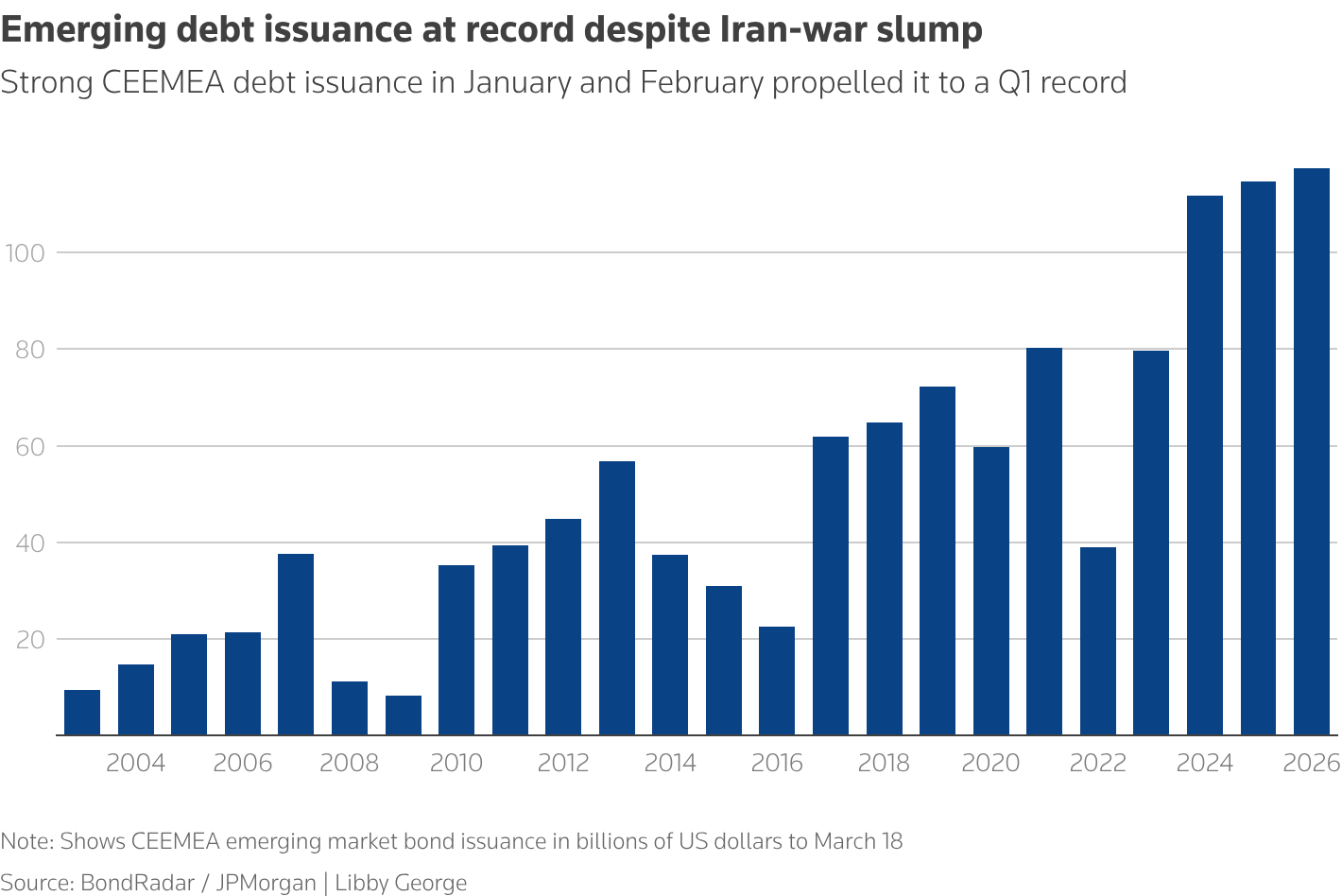

Emerging nations, led by Saudi Arabia, Mexico and Turkey, had issued credit in January and February at such a surprising pace that first-quarter sales were a record despite a lack of output in March, according to Stefan Weiler, JPMorgan’s head of CEEMEA credit markets.

Independent and corporate investors in the central and eastern Europe, Middle East and Africa (CEEMEA) had raised about $ 117.5 billion, about $ 3 billion above the first three months of 2025, even before Angola came to the market this week.

Angola is one of the few emerging powers whose debt has grown since the US-Israeli campaign against Iran began on February 28, Mourad said, a sign that investors are now demanding a smaller loan payment to the West African oil-producing country than before the war.

Africa-focused investment firm Helios Towers also issued a loan this week.

For others, the picture is more difficult: investors pulled $3.3 billion from emerging debt in the week to March 19, and more than $5 billion from high-yield commercial bonds, according to Bank of America. The latest marked the biggest move since the US rate hike in April 2025, the bank said.

Credit extensions for the likes of Egypt and Turkey have increased due to the impact that the war could have on their economies – as has some of Saudi Arabia’s oil – and the first two countries are also at great risk of rising energy and food costs.

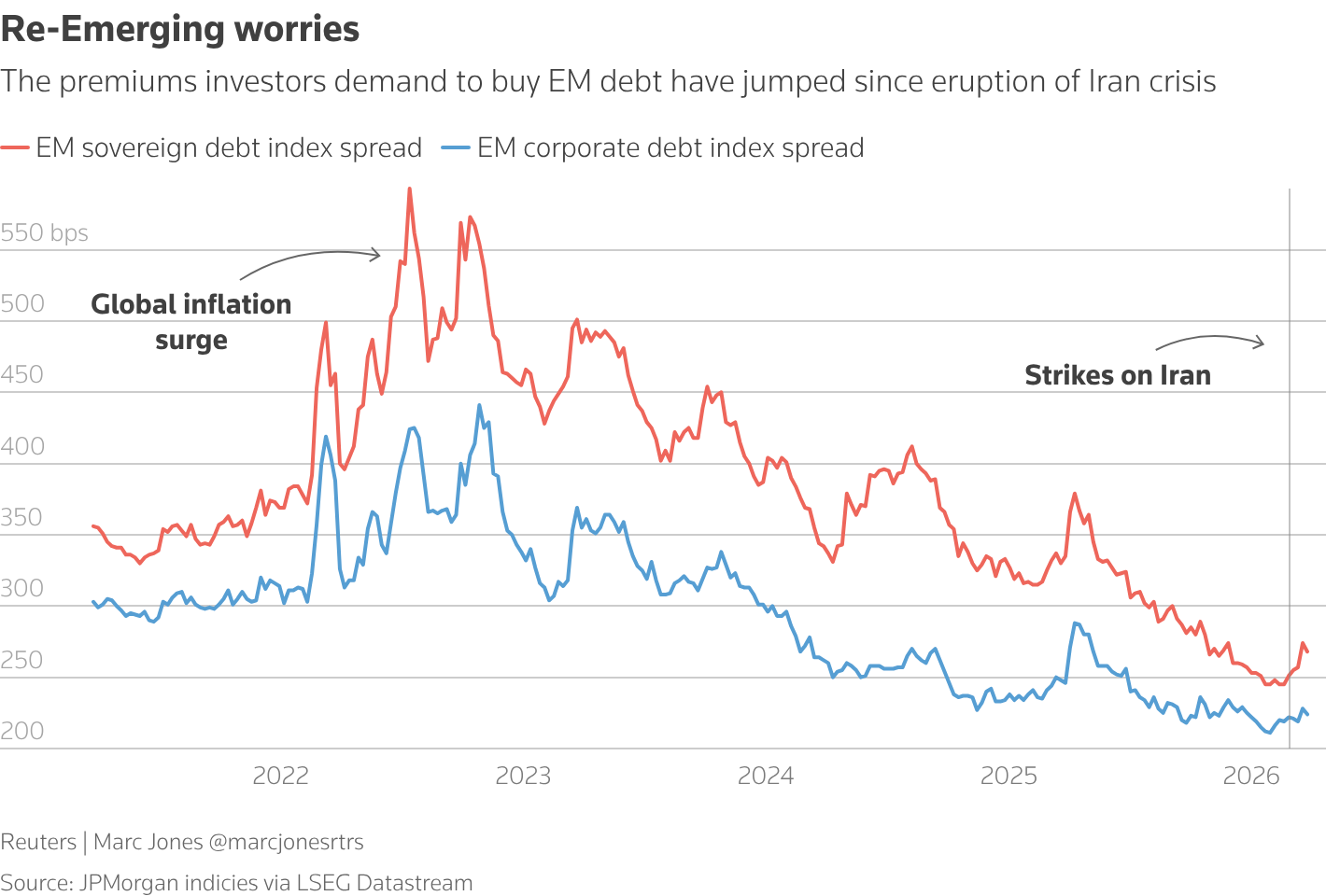

The JPMorgan EMBI spread between emerging dollar debt and US Treasuries widened by 17 points, to 268 bps, since the end of February, while Egypt’s 44 bps and Turkey’s widened by 36 bps.

Angola, at the same time, decreased by 39 bps to 504 bps.

The unpredictable nature of the conflict – with unprecedented attacks on the energy resources of the Gulf countries and the closure of the important Strait of Hormuz – has led to the attention of investors to take large positions in many assets.

But several banks have specifically reduced their overweight positions for emerging markets.

“The only major change we’ve made since the start of the war is to increase our holdings and reduce our weighting of holdings going forward,” said Manish Kabra, multi-asset strategist at Societe Generale.

For Weiler, a few successful deals in the pipeline could spark “more deals waiting to happen.”

“Private negotiations are often more attractive or desirable to borrowers during market downturns,” Weiler said.

A STRONG THING AWAITS ON THE MAPS

Meanwhile, Weiler and Mourad said investors have been buying Gulf sovereign debt in secondary markets, highlighting potential demand as tensions ease.

“We’re getting more questions from investors, especially about high-profile names — especially sovereigns,” Weiler said of the debt of Gulf states like Saudi Arabia.

Mourad said the secondary credit markets were not coping with the turmoil.

“The fact that investors are buying the current values in the second place gives an indication that the interest is continuing,” he added: “The widening (spread) that we have seen, for some, is a good entry point.”

Reported by Libby George and Reuters. Additional reporting by Dhara Ranasinghe and Karin Strohecker; Graphic by Marc Jones; editing by Andrei Khalip

Our standards: The Thomson Reuters Trust Principles.

#Emerging #market #debt #falling #Iran #war #drags #markets