Patient Capital, Long-term Attitudes and Global Inequality: A Controversy

Written by Yan Wang

The world economy in early 2026 is facing an escalating conflict in the Middle East that is causing humanitarian and energy crises. In terms of economics, although there is agreement that global inequality is increasing, there is no concrete evidence of the causes of this inequality. The IMF’s 2025 Article IV consultation with China, concluded in February 2026, indicates that China’s economy remains generally stable, but its current growth pattern faces significant internal and external imbalances. The IMF’s main recommendation is to push China towards consumption-led growth, reduce investment inefficiencies and maintain immunity through structural reforms.

Although the above analysis has merits, the report fails to deal with the other side of the world’s imbalances, namely, low savings and very high deficits that lead to the rapid expansion of government debt in some G7 countries, especially the United States. Chinese economists question the fairness of the IMF blaming China for global imbalances. For example, 250 years of historical data provided by John Ross (2026) confirms that China’s high level of investment is not a sign of distortion or imbalance, but one of the main reasons for the country’s sustained long-term growth.

There is an argument to be made that contradicts the IMF’s criticism of China’s high savings rate, by asking whether it is desirable or reasonable to reduce China’s high savings rate, based on the Chinese tradition of “long-term outlook” (LTO), which is part of China’s soft power. From the perspective of financing gaps for green development and building a sustainable future, is it a good idea to lower China’s savings rate? Here’s a friendly warning: “don’t throw the baby out with the bathwater.”

Patient Care as a Comparative Advantage

Nine years ago, the paper showed that the IMF’s encouragement of financial account liberalization is misleading. In fact, capital, like labor, has never been the same. Some capital is “patient capital,” while other capital is highly mobile, or “footloose,” which can leave the country at any time. Africa has been suffering from financial flight in the tens of billions of US dollars every year according to Ndikumana and Boyce 2011.

The proposed concept was “patient capital,” based on the LTO of the country or region, as well as the development of institutional investors in the banking and financial sector. Patient money was broadly defined as money to be invested in a relationship where the lender is willing to see the borrower grow in the future to make a profit. This includes parents investing in their children’s education, government funds for investment in new institutions, and entrepreneurs investing in unlisted equity in infrastructure projects. These investments are not intended for short-term profit but for long-term future profit when the loans or invested projects increase. The owners of this patient capital are equity investors, who are more willing and in a better position to take risks.

Previous studies have shown LTO as a result of pre-industrial agricultural climates that were conducive to higher returns on agricultural investment. It is a kind of cultural gift because it is rooted in a thousand-year history of agricultural development and the Confucian cultural background that values persistence, patience, thrift, and the ability to adapt and learn. A long-term perspective has been considered beneficial to the creation of human and physical capital, technological progress and economic growth. For example, a growth commission report found that “future learning is associated with higher levels of savings and public and private investment.”

LTOs and savings are not the same as patient funds. Family savings for retirement, parents saving for their children’s education, and residents building wealth for the future are all sources of long-term income. However, high retention rates alone are not enough. Institutions are important to implement the hidden benefit of the savings comparison. Only when the country produces financial institutions that are able to provide long-term financing and find cheap and reliable money as a source of funds can the patient’s money be found. In other words, the country may have a long-term trend and save money, which is a “hidden comparative advantage.” But it is only when banks, pension funds, sovereign wealth funds, and development finance organizations are doing well that this latent opportunity becomes a comparative revealed opportunity. However, the hard truth is that many developing countries are often underperforming when they use strategies that work against their comparative advantage. These policies can lead to an unstable business environment, financial burdens, inflation, financial stress, and external imbalances.

Long-Term Attitudes and Trends in International Investments on the Internet

Now, the important question is which countries and regions have LTO and the ability to turn it into patient capital, and how it can be measured. Based on the work of Hofstede and his colleagues, and the LTO index found based on the World Values Survey data collected by Misho Minkov (2007), Geert Hofstede and his co-authors, and published in the book entitled “Cultures and Organizations: Software of the Mind.” Another variable was also used––Net International Investment Position (NIIP)––as a proxy for a country’s patient income invested abroad, although it is not an absolute measure due to the focus on financial assets and liabilities.

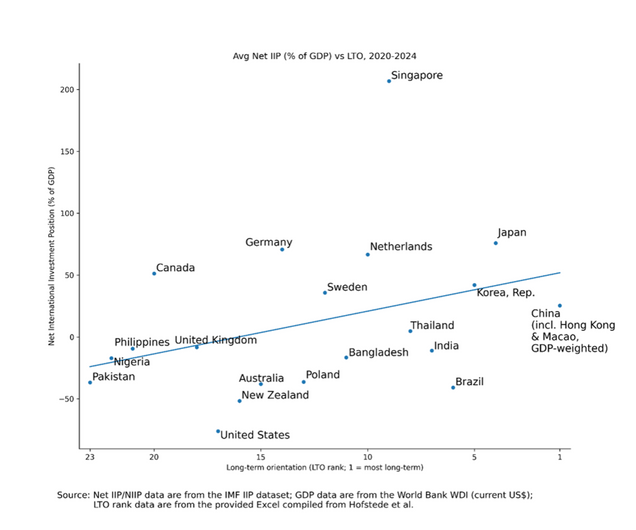

Figure 1: Relationship between international investment levels (as % of GDP) and long-term outlook (LTO), 2020-2024

A robust correlation analysis shows that the average Net IIP in 2020-2024 is positively correlated with the LTO index (as shown in Figure 1). In other words, countries with a strong LTO, especially East Asian economies, are more likely to develop a strong external debt position. This is consistent with the work of the Growth Commission (Spence 2008), and many East Asian economies including Japan, South Korea, Taiwan, Hong Kong, China, and Singapore, have similar long-term orientation characteristics. The resulting hypothesis is that the NIIP of these economies may be higher than those without LTO. If this hypothesis can be further studied and confirmed by other evidence, such as Net FDI (outflows minus inflows) and cross-border M&A, we can assume that this economy has a revealed comparative advantage for the benefit of patients as described above.

On the other hand, countries with short-term expectations and low savings rates will see their Net IIP, or foreign investment positions, deteriorate along with their foreign liabilities. The US used to have a very good NIIP in the early 1980s, but by 1990 it had become the world’s largest creditor. By the end of Q3 2025, the US debt level had dropped to USD $-27 trillion, with assets of USD $41.27 trillion and liabilities of USD $68.89 trillion. Despite the important recognition that there is high foreign demand for USD-denominated assets, the decline in the US NIIP still means that it is absorbing more of the world’s reserves than it is supplying to the rest of the world. For many countries in the Global South that are in dire need of dollar financing, China’s efforts to use up its trade surplus (about USD $1.2 trillion by 2025) through the Belt and Road Initiative and similar programs, provide an important source of long-term financing.

China Uses Its Comparative Advantage in Patient Capital

The IMF mainly makes recommendations from the point of view of balancing and expanding consumption, but this way of thinking does not take into account the deep cultural and institutional foundations that support China’s high savings rate. China’s high savings cannot be fully explained by the characteristics of saving and earning culture, but it is largely based on the cultural history of LTO, and the institutional conditions for the creation of patient income. The cultural definition may seem slippery, but ultimately it is about how individual families, as well as the community as a whole, perceive danger. In successive quality surveys, China’s LTO index has remained at the top. It is precisely this LTO, together with institutional arrangements that are able to transform long-term savings into investment power, that has helped China and other neighboring countries in East Asia with a strong Confucian tradition to work harder to finance construction and long-term project investments, than countries that are weak for a long time.

We believe that NIIP can serve as a useful proxy for measuring a country’s ability to sell money. A positive NIIP indicates that the country has achieved a relatively strong export position. On the other hand, countries with a strong short-term tendency and low savings rates are more likely to face the deterioration of their external positions and accumulate large amounts of foreign debt.

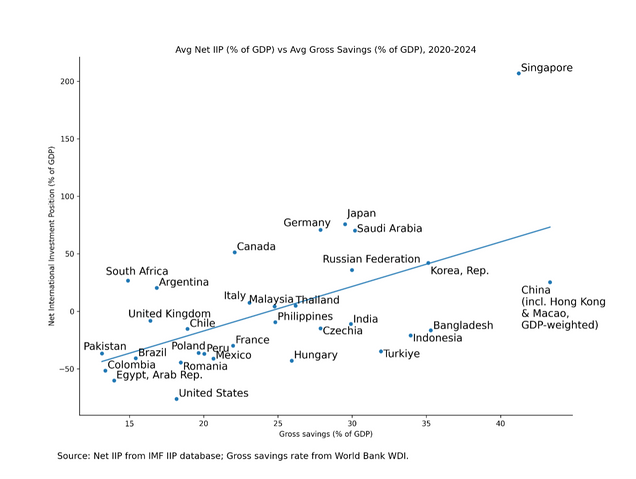

Figure 2: Relationship between international investment levels (as % of GDP) and total savings (as % of GDP), 2020–2024

As shown in Figure 2, the data for 2020-2024 also confirms that a high savings rate is significantly related to a good level of international investment, and this relationship is positive and statistically significant. Although China is still developing as a country, it has grown to become a major financial exporter in recent years. This phenomenon, called the “Lucas Paradox” (capital flowing from developing countries to developed countries), can be explained by LTO: China has a unique sense of tolerance that is proven by its success under China’s five-year plans, which is in its 15th year.th edition from 1953. This patient income can be used as an opportunity for comparison under certain institutional conditions, although further analysis is needed.

For China, balancing spending may be necessary, and establishing a more comprehensive social security system may help reduce excessive defense spending. However, in this process, the power of patiently collecting and investing long-term capital should be protected as an opportunity to compare with the source of soft power.

This represents a policy warning: policymakers should be cautious and avoid undermining the institutional and cultural foundations that make the patient more profitable. Due to the large financial gaps to close the digital divide, green development, and fight climate change, more long-term international investments are needed. This also includes a serious discussion about the imbalances of the world: the international community, including the IMF, should hold great power to high standards to build bridges and public goods of the world, instead of destroying or discarding what is really important during rebalancing.

*

#Patient #Capital #Longterm #Attitudes #Global #Inequality #Controversy