Average ARMs have started to drop further and are at record lows: FHFA’s National Mortgage Database.

By Wolf Richter for WOLF STREET.

The extremely low mortgage rates for 2020 to 2022 – the 30-year rate has fallen below 3% as inflation is heading towards 9% – is one of the reasons for this frozen housing market, where housing sales have already fallen by almost 25% since 2019, and consumption has fallen for the third year after 5%. as of 2019. Homeowners who financed and refinanced a home with those low mortgage rates back then and now want to move and buy another home would be hit with very high mortgage rates and very high prices, and for many the numbers are incomprehensible, and they always are. So we watch those loans for signs of meltdown. And there is a thaw, but very slow, and slow.

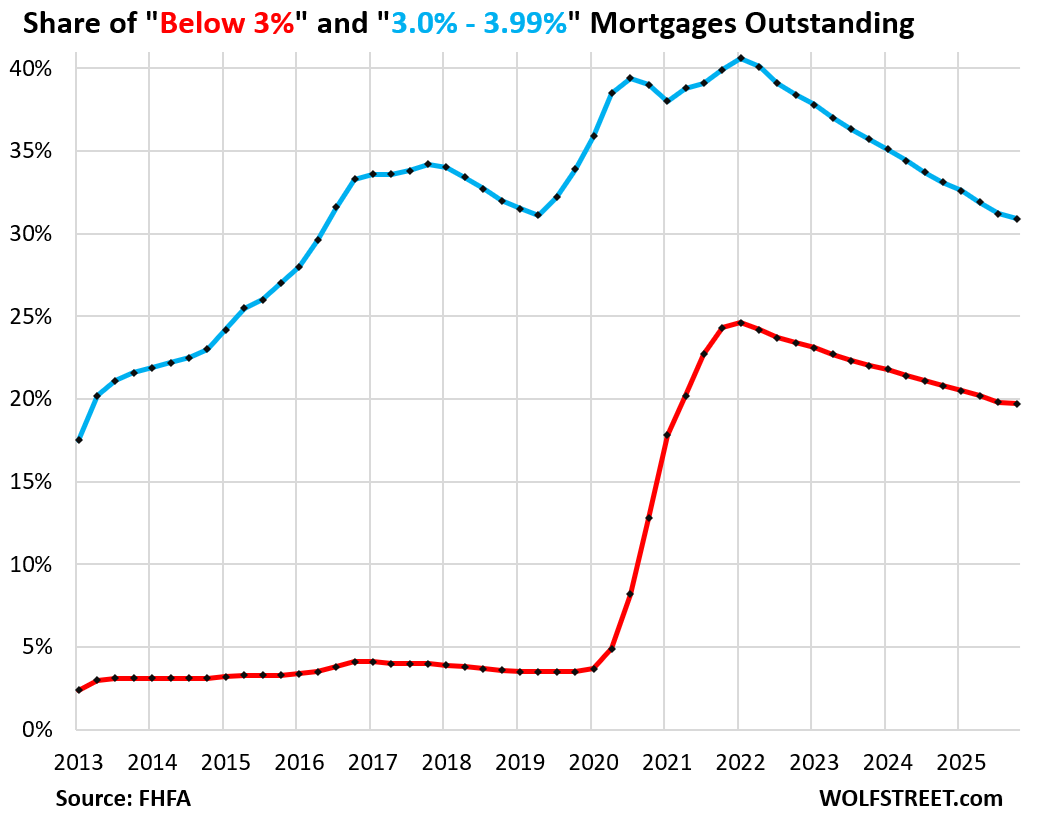

The share of less than 3% outstanding loans, by the number of loans (red line in the chart), fell to 19.7% of all outstanding loans in Q4 – progress that is already slower than ever – down from a share of 24.6% at the peak of Q1 2022, according to data from FH Hous Agency today. The data station goes back to 2013 only.

The share of loans from 3% to 3.99% (blue) fell to 30.9% – the slow progress also slowed – down from the 40.6% share at the peak of Q1 2022.

The share of mortgages below 3% exploded from the beginning of 2020 until Q1 2022 when the Fed cut interest rates – policy rates close to 0% and billions of dollars of bond purchases, including mortgage-backed securities (MBS) – created a tsunami of homeowners renovating their new homes to get interest.

And now they are very reluctant to give up those mortgage payments. But life happens – death, divorce, an unstoppable new job, addition to the family, the desire to be closer to the children, etc. – and families are sold and mortgages are paid off, and those very low mortgage rates are still falling in the housing market, but at a snail’s pace.

All types of mortgages are included here, such as 30-year fixed-rate mortgages, 15-year fixed-rate mortgages, and Variable Purchase Loans.

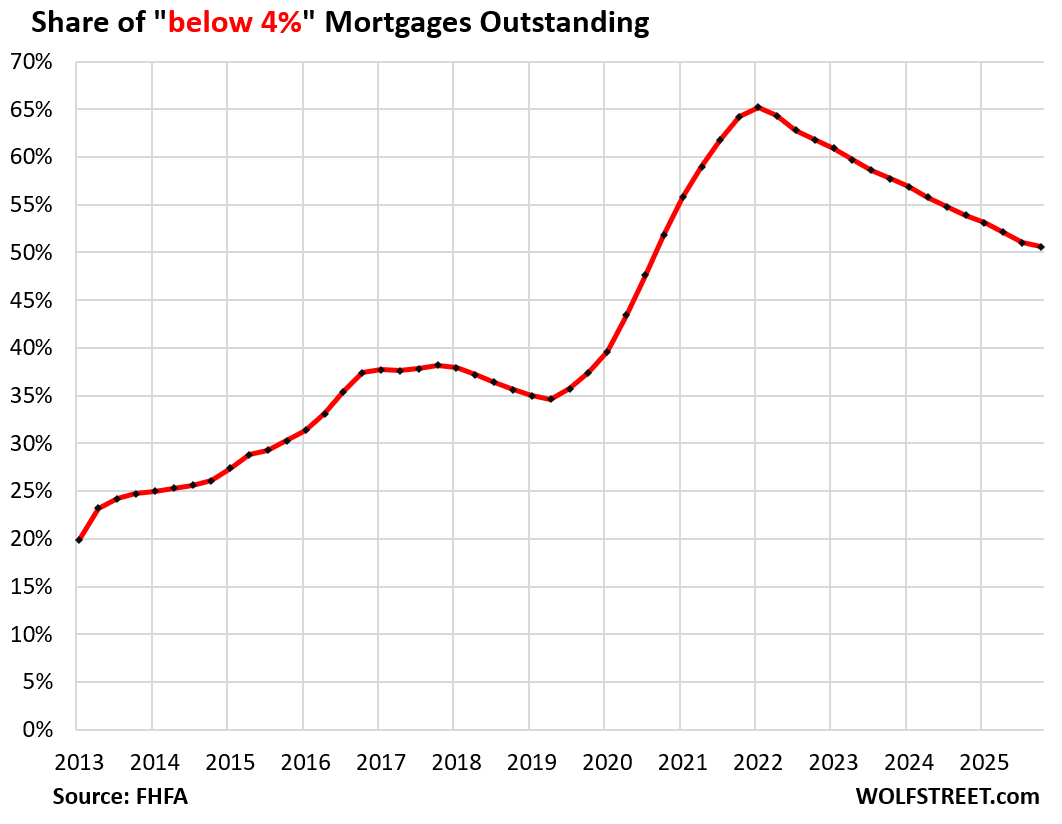

Combined, the portion is less than 4%-mortgage decreased to 50.6% of total outstanding loans. At the peak of Q1 2022, more than 65% of all loans outstanding had an interest rate of less than 4%.

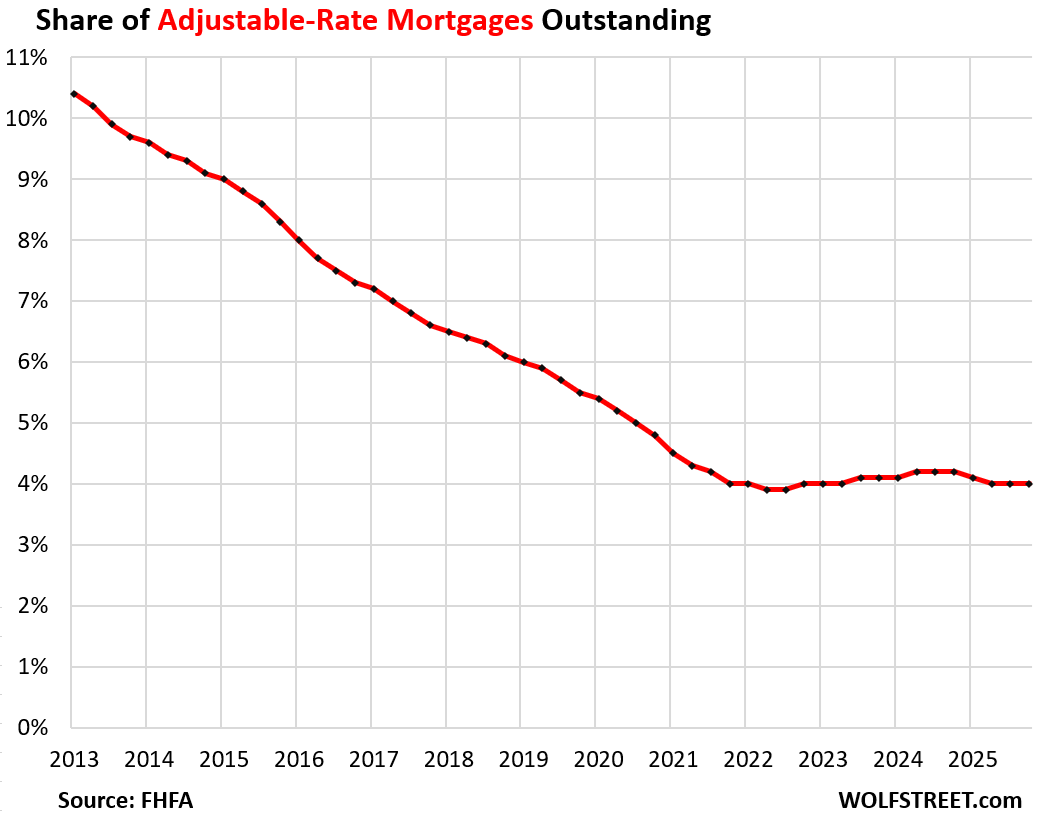

Adjustable-Rate Purchase Loans outstanding has been at its lowest level since 2021, and is still at 4.0% in 2025, down from more than 10% in 2013, most of the FHFA notes.

Some ARMs had rates below 3% even before 2020, which is one of the reasons why mortgages below 3% (red line in the chart above) were between 2.5% and 4% before 2020.

Homeowners with ARMs that originated when rates were low face the fear of payments as their mortgage rates change when rates begin to rise in 2022.

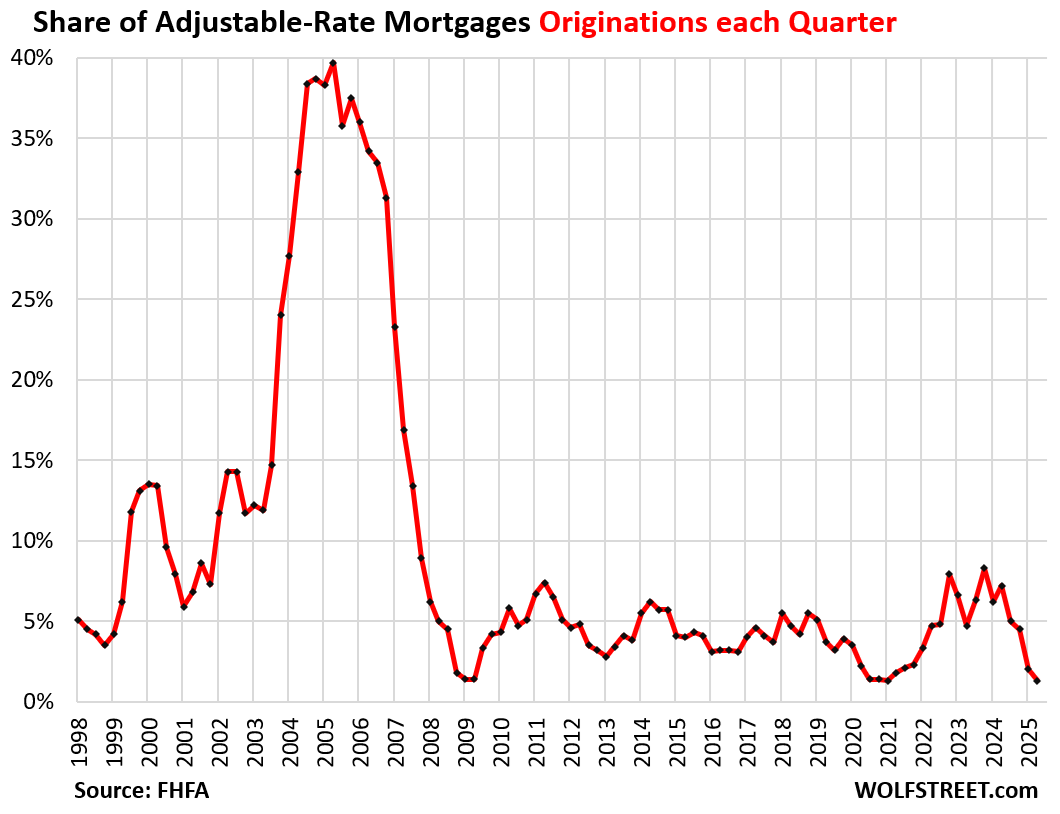

The origin of ARMs (new ARMs issued per quarter) remain low and will continue to decline, despite the ridiculously silly articles in the crisis media exists be the next big wave of ARMs.

In Q2, the most recent data available from FHFA, the share of ARM originations fell to 1.3% of total loan originations, among the lowest share recorded in FHFA data on ARMs, going back to 1998. But note the ARM bubble during Housing Bubble 1:

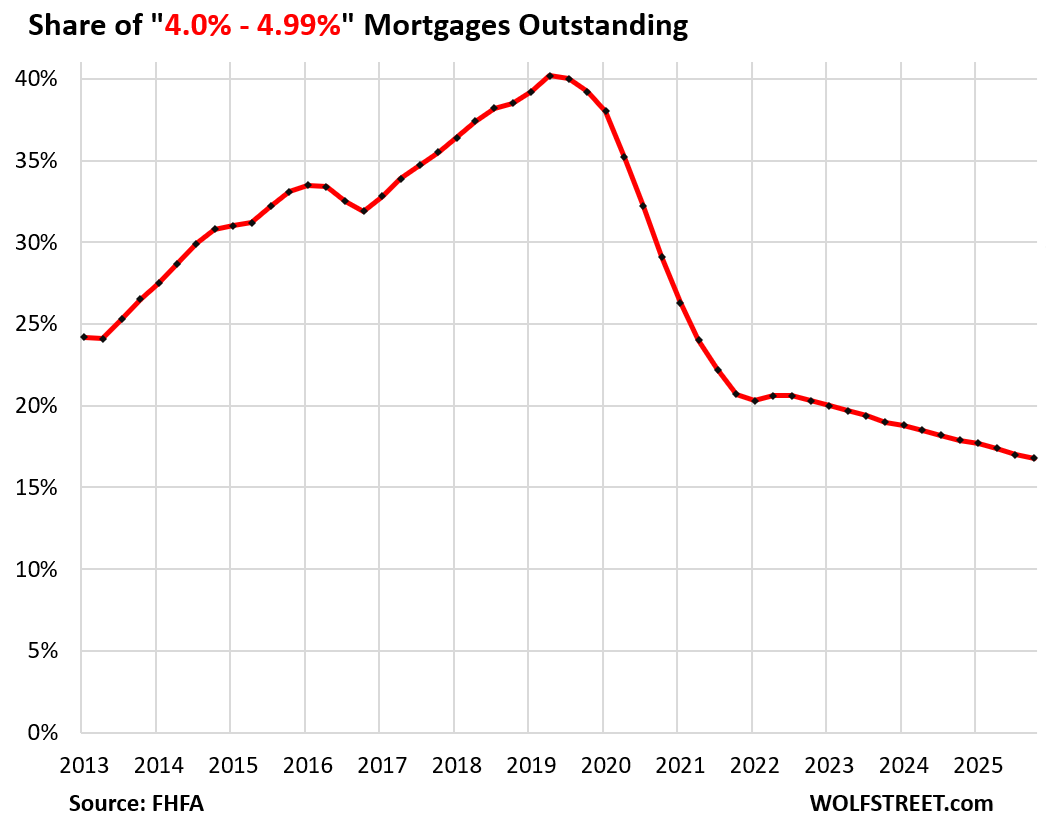

4.0% to 4.99% mortgage rate fell to 16.8%, the lowest share in FHFA data going back to 2013, and down from a 2019 peak of 40%.

Homeowners who qualified for mortgage rates between 4.0% and 4.99% before 2020 were upgraded to very low-cost loans. In other words, they were funding come out of this portion of 4% to 5%, that’s why the remaining amount of those loans has decreased in 2020 onwards.

But homeowners who had 6% or 7% mortgages before 2020, because of lower credit scores and other factors, also got refinanced mortgages at much lower rates, and many of them were refinanced. to enter this group of 4% to 5%, that is why the share of this group did not go down more than it did.

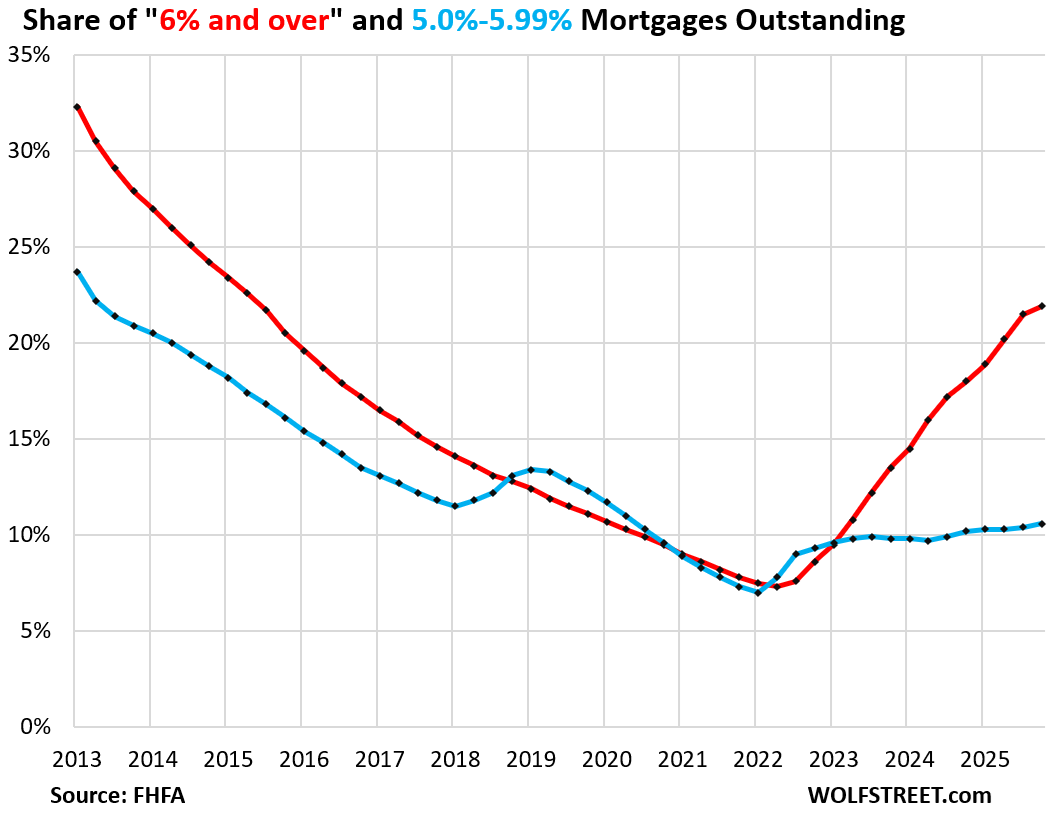

5.0% to 5.99% mortgage rate held up to 10.6% in Q4 and has been at a two-year high (blue in the chart below).

There are now fixed rate loans offered in this type, including 15-year mortgages, but 15-year loans are less popular because the payment is higher.

6% share-plus mortgage rose to 21.9% of all loans in Q4, the highest since 2015, from a low of 7.3% in Q2 2022 (red in the chart).

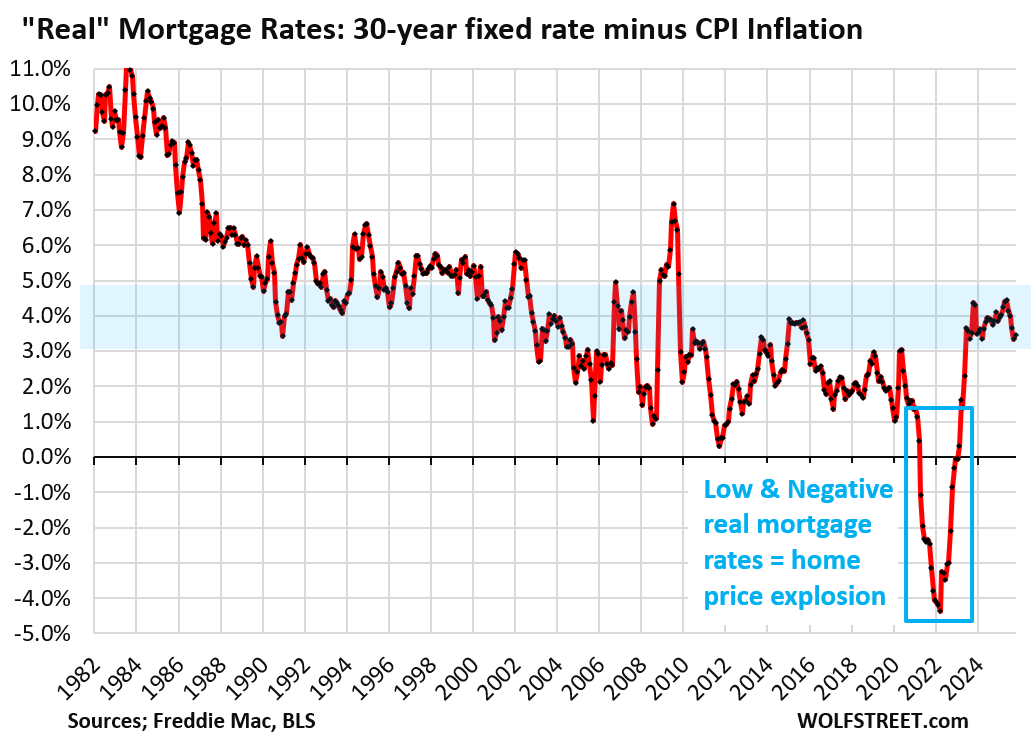

What exploded the housing market. In the early 2020s, as the Fed put in place its loose monetary policies, including buying billions of dollars of MBS to lower mortgage rates, the 30-year fixed rate fell and eventually settled below 3%, even as inflation rose. At the beginning of 2022, the 30-year average of fixed mortgage rates was below CPI inflation: negative “real” mortgage rates (mortgage values do not decrease CPI inflation). This was better than free money!

At the height of the Fed’s recklessness, the 30-year average inflation rate was less than 3% and the CPI inflation rate reached 7%, and “loan rates (minus CPI inflation) were 4 percent below CPI – minus 4% of real mortgage rates. This is what blew up the housing market, caused a huge explosion in home prices,’ and caused significant long-term damage that continues to damage the housing market and will take years to repair.

Enjoy reading WOLF STREET and want to support it? You can give. I really appreciate it. Click on the box to find out:

![]()

#Lockin #Effect #Improvement #Housing #Market #Sub3 #Home #Loans #Slowing